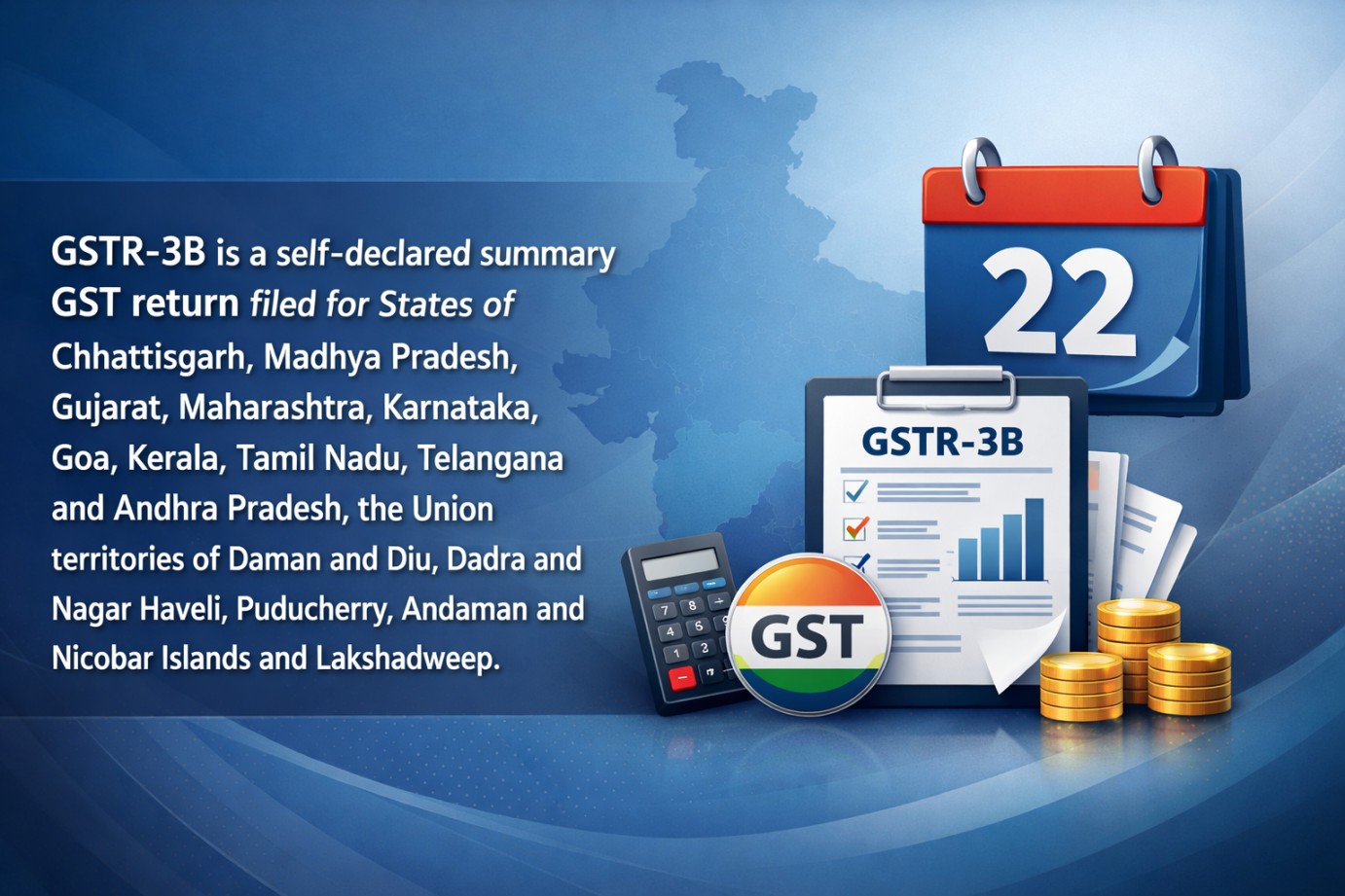

GSTR-3B is a self-declared summary GST return filed

GSTR-3B Due Dates for Selected States & Union Territories – Key Compliance Guide

GSTR-3B is a self-declared summary GST return that must be filed by registered taxpayers to report outward supplies, input tax credit (ITC), and tax liability. Timely filing is essential to avoid penalties and ensure smooth compliance.

Applicability of GSTR-3B Due Dates

Under the GST framework, the due dates for filing GSTR-3B vary based on the taxpayer’s turnover and state/UT classification. As per Rule 61 of the CGST Rules, 2017 and relevant notifications issued by the CBIC (Central Board of Indirect Taxes and Customs), taxpayers are divided into different groups for staggered filing.

The following States and Union Territories fall under the category where GSTR-3B is generally due on the 22nd of the succeeding month (for quarterly filers under QRMP scheme):

-

Chhattisgarh

-

Madhya Pradesh

-

Gujarat

Need help with this? Talk to Tejash Joshi & Co → -

Maharashtra

-

Karnataka

-

Goa

Need help with this? Talk to Tejash Joshi & Co → -

Kerala

-

Tamil Nadu

-

Telangana

-

Andhra Pradesh

-

Union Territories:

-

Daman and Diu

-

Dadra and Nagar Haveli

-

Puducherry

-

Andaman and Nicobar Islands

-

Lakshadweep

-

This classification is based on notifications such as Notification No. 85/2020 – Central Tax dated 10-11-2020, which introduced staggered due dates to ease compliance burden.

Who Needs to File GSTR-3B?

GSTR-3B must be filed by:

-

Regular GST-registered taxpayers

-

Taxpayers under the QRMP (Quarterly Return Monthly Payment) scheme

-

Businesses reporting summary details of:

-

Outward supplies (sales)

-

Input tax credit (ITC)

-

Tax liability and payment

-

Key Compliance Points

-

Due Date (Monthly Filers): 20th of the following month

-

Due Date (QRMP Scheme):

-

22nd or 24th of the following month, depending on state grouping

-

-

Late Fees: ₹50 per day (₹25 CGST + ₹25 SGST), subject to limits

-

Interest: 18% per annum on delayed tax payment as per Section 50 of the CGST Act, 2017

Why Timely Filing Matters

Filing GSTR-3B on time ensures:

-

Avoidance of late fees and interest

-

Continuity of input tax credit

-

Smooth GST compliance rating

-

Avoidance of notices from the department

Conclusion

Understanding the correct due date based on your state is crucial for GST compliance. Businesses operating in the above-listed states and union territories should particularly note the 22nd due date under the QRMP scheme.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from Tejash Joshi & Co. Reach out to discuss your requirements.